Welcome to your roadmap to homeownership! If you are dreaming of holding the keys to your own home in Jamaica, the National Housing Trust (NHT) is your most powerful partner. I am here to break down exactly how you can turn those weekly paycheck deductions into the foundation of your future home.

Let’s dive deep into how the NHT works, what you qualify for, and the hidden strategies you can use to maximize your buying power.

The Basics: Do You Qualify?

Before you start scrolling through real estate listings, you need to ensure you meet the basic NHT criteria. To qualify for a home loan, you must:

- Be between the ages of 18 and 70.

- Earn at least the Jamaican minimum wage.

- Have made a minimum of 52 weekly contributions to the Trust.

- Be actively contributing, meaning you have made at least 13 weekly contributions in the 26 weeks directly leading up to your application.

If you are self-employed, don’t worry—you can still qualify! You just need to ensure you are registered, filing your estimated (S04A) and actual (S04) annual returns, and making your quarterly payments at Tax Administration Jamaica (TAJ).

Your First Step: Always start by requesting your Eligibility Letter online. This document is your golden ticket. It tells you exactly how much you can borrow, your specific interest rate (which is based on your income and ranges from 0% to 5%), and your repayment timeline.

Choosing Your Path: Buy, Build, or Scheme?

The NHT doesn’t just offer one type of loan. Depending on your goals, there are several distinct paths you can take:

Buying an NHT Scheme Unit:

The NHT frequently builds housing developments across the island. To buy one of these, you have to apply when a scheme is advertised. Selection is highly competitive and is based on a points system. You earn 20 points for every 52 weeks of contributions you’ve made, plus an additional 70 to 110 points depending on your income bracket.

Buying on the Open Market:

If you want to buy a house from a private developer, a real estate agent, or an individual seller, you will use an Open Market Loan. You can borrow up to $9 million as a single applicant. However, there is a crucial rule here: if you earn more than $30,000.99 per week, you cannot process this loan directly at an NHT branch. You must apply through a partner bank, building society, or credit union under the External Financing Mortgage Programme (EFMP). The great news is that you will still get the low NHT interest rate on the NHT portion of your loan.

Building on Your Own Land (BOL):

If you already own a piece of land with a registered title, a single applicant can borrow up to $11 million to construct a house. Don’t own land yet? The NHT offers a “Buy Land & Build” loan, where you can use up to $5 million of your entitlement to purchase the land, and use the remaining balance to build the house.

Pro Strategies: Maximizing Your Purchasing Power

Houses are expensive, but the NHT has built-in mechanisms to help you afford more.

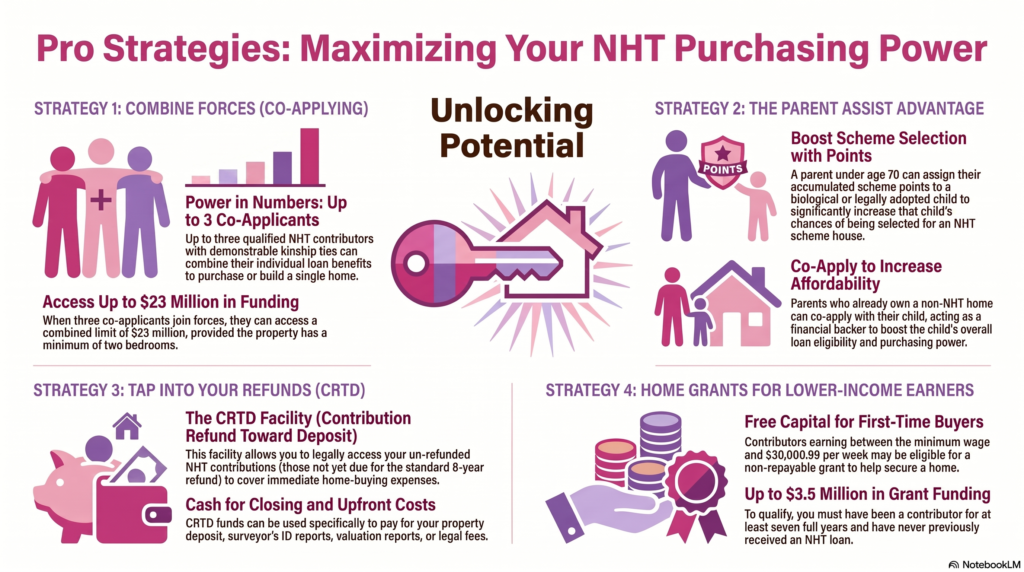

- Combine Forces (Co-Applying): You don’t have to do this alone. Up to three qualified NHT contributors with demonstrable kinship ties can combine their benefits to buy or build a home. Together, three co-applicants can access up to $23 million, provided the house being purchased or built has at least two bedrooms.

- Parent Assist: If you are a young person trying to get your foot in the door, your parents can help. A parent under the age of 70 can assign their accumulated scheme points to a biological or legally adopted child to massively boost their chances of winning an NHT scheme house. Parents who already own a non-NHT home can also co-apply with their child to boost their affordability.

- Tap Into Your Refunds (CRTD): Struggling to find the cash for a deposit or closing costs? The Contribution Refund Toward Deposit (CRTD) facility allows you to legally use your un-refunded NHT contributions to pay for your deposit, surveyor’s report, valuation report, or legal fees.

- Home Grants: If you earn between the minimum wage and $30,000.99 per week, and you have been contributing for at least seven full years without receiving a loan, you may be eligible for a Home Grant of up to $3.5 million to help you secure a home.

- Beware of the Hidden Costs

The purchase price is not the final price. When budgeting for your home, you must factor in the additional expenses. You will need to pay a property valuator and a commissioned land surveyor. Furthermore, be prepared for legal fees (attorneys usually charge around 3% of the selling price plus GCT), stamp duty, and registration fees. Finally, note that the NHT charges a service charge of up to 5% of the loan amount to cover administrative and legal processing, though this is usually added to your mortgage balance.

Your journey to homeownership is a marathon, not a sprint. Take it one step at a time, starting with that Eligibility Letter.

Leave a Reply